On the verge of closing 2021, it can already be said that this year, in the Spanish and European thermoplastic industry, we will remember it especially because of the constant increase in prices and the scarcity of material. Not to mention long production and delivery times and sometimes with product restrictions.

The reasons that have caused this anomalous situation are:

- Constant Increase in the price of raw materials due to the lack of imports.

- In Europe, manufacturing stoppages of thermoplastics due to incidents in production plants.

- Permanent increases in the cost of energy.

- Logistical problems on a global scale. Increase in shipping costs.

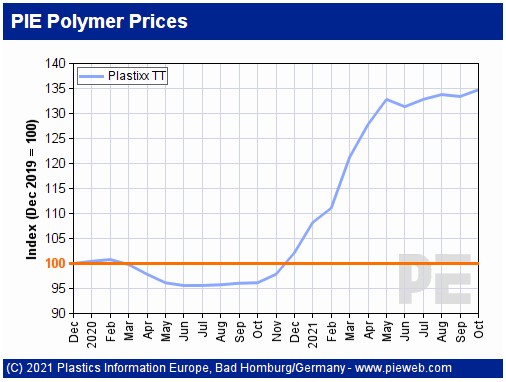

Table that reflects the price behavior of engineering thermoplastics in Western Europe, from December 2019 (pre-pandemic) to October 2021 (post-pandemic).

Increase in the price of raw materials

Over the course of this year, there has been an imbalance between supply and demand for short-term commodities. Europe is a net importer of polymer raw materials and is therefore vulnerable to market disturbances.

Over the course of the year, we had to face a scenario of decline in imports of raw materials (both Asian and to a lesser extent American), necessary for production, which has caused the impossibility of immediate supply of many materials, causing supply cuts.

The hope of a few months ago, faced with this reality, was that over time the situation would normalize and the growing Asian demand would be contained, but as of today the situation has not yet stabilized, on the contrary, the situation is still unstable and this autumn companies such as: Trinseo, Clariant, Songwon Wacker, Archroma or Lanxess have announced increases.

The European plastics converters association, European Plastics Converters (EuPC), warns of the risks that the private interests of many raw material companies can cause to the industry as a whole.

Production stoppages in European thermoplastic factories

To everything mentioned in the previous point, we have added the multiple stoppages of production by different European manufacturers. On this occasion, in addition to the usual production cuts to carry out annual maintenance plans, forced cuts have been added due to declarations of force majeure (FM).

Cases such as PVC, which had already had 7 FM in mid-September, have significantly reduced European production capacity.

But it must be said that, even returning to full productive capacity, after the reopenings, the volumes produced will not be sufficient to compensate for the lack of imports suffered.

Permanent increases in the cost of energy

At present, the global energy situation does not seem to help contain prices and a normalized supply of supply.

This year there have been several extreme weather events, which have had direct consequences on global energy costs.

Examples include a longer than usual winter in Europe, a heat wave and a drought last summer in China or states of emergency in the southern states of the USA (Texas and Louisiana). The latter have been caused by hurricanes Ida and Nicholas, which have caused serious damage to oil refinery infrastructures. As a result, cuts in U.S. oil production are significant, and its exports have declined considerably.

To all this, add an energy crisis that is affecting China in a very important way. Caused by:

- Lack of coal supplies.

- A greater tightening of the country's regulations on greenhouse gas emissions, with the objective of complying with China's international environmental commitments.

- A strong energy demand from the industrial sector, to avoid production cuts.

Not to mention, the high cost of electricity in Europe, which has already become a direct price factor.

As a result, the lack of energy raw materials (oil, natural gas, etc.) is causing many European polymer suppliers to consider the direct application of energy surcharges.

Logistical problems on a global scale

After a very turbulent year in terms of shipping costs, it seems that at this time, freight costs tend to stabilize upwards and show a slight decline, after reaching relative highs a few weeks ago. In the last month, reference values for the price of shipping, such as the Baltic Dry Index, have fallen sharply. Prices, despite the recent trend, are still at maximum levels compared to those at the beginning of the year.

In general, over the year, as a result of the increase in demand following the end of the pandemic, there have been bottlenecks in the raw materials market, as it has not been possible to respond immediately to the demand generated. All of this has resulted in a general increase in prices.

In the short term, the situation is not expected to rectify, and large investment banks, such as Goldman Sachs, state that the market is complacent with their expectations since they predict that the increases will last longer than expected at first.

Sources:

- Spanish Association of Plastic Industrialists.

- European Plastic Transformers Association.

- Baltic Exchange Dry Index (BDI)

- Mundo Plast

- Plastics Information Europe (PIE)

- Refinitiv Datastream